At an office building in San Francisco’s Mission District, a small group of people that just met sat pondering how much money to give to each other — between $50 and $200 per month.

One by one, a bus driver, a science teacher and others around a table said “200,” until Jazzel Woods Sr.’s turn came up.

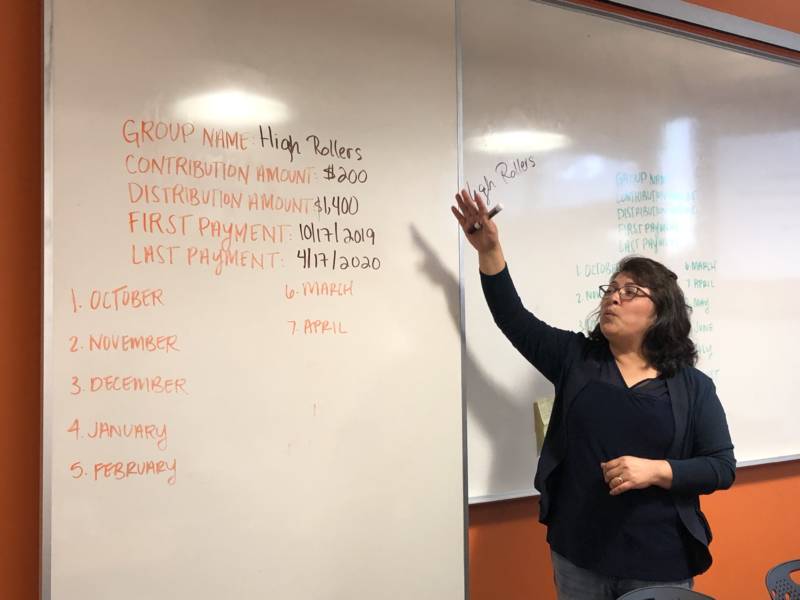

“Oooh! You all some high rollers!” said Woods, 28, a teen counselor in Oakland who is struggling to pay his rent. After some hesitation, he said: “Yeah, I can give you 200.”

Woods and the other Bay Area residents are committing to participate in a program that bridges informal traditional lending practices — called tandas in Mexico or kye in Korea — with the mainstream financial system.

The nonprofit Mission Asset Fund, which manages the program, guarantees participants zero-interest loans and the chance to build their credit scores, which helps build financial stability.

While MAF’s lending circles were initially focused on low-income Latino immigrants in San Francisco’s Mission District, the program has become a tool to boost credit scores for African Americans, young people and others across the country.

About 45 million adults in the U.S. have no or insufficient credit scores, which often shuts them out of more affordable mortgage, car and business loans and other bank financial products. Those consumers, who are disproportionately black, Latino or low-income, tend to resort to expensive payday lenders to borrow money, which can then eat up their income.

More than 3 million people in the Los Angeles, San Francisco, Riverside and San Diego metropolitan areas have no or insufficient credit scores, according to estimates by the Consumer Financial Protection Bureau.

It’s a Catch-22: To get good credit, consumers must first have good credit scores.

“We knew that that was a big problem for folks in the immigrant community,” said José Quiñonez, who founded Mission Asset Fund. “But what we realized was that, well actually, they have this other really rich way of managing their money. It just wasn’t connected to the formal financial system.”

(Farida Jhabvala Romero/KQED)

To help people access better credit, Quiñonez adapted an age-old system of friends or relatives pooling resources to give each other loans, and added a system to report those loan repayments to U.S. credit bureaus — that adaptation is considered by some a groundbreaking innovation in microlending.

Participants in MAF’s program sign formal agreements that allow the organization to electronically withdraw a set amount monthly from their bank accounts and rotate who gets the collective pot of money each month. As MAF reports borrower payments, researchers found their credit scores can significantly increase, particularly for those who had no credit scores to begin with.

“Getting a $1,000 loan with zero interest is awesome. But the real life changing component to our work is helping people build their credit,” said Quiñonez, who chaired the Consumer Financial Protection Bureau’s consumer advisory board from 2012 to 2015. “Because a good credit score opens up doors for a world of possibilities for people in the financial marketplace.”

Quiñonez and MAF have helped raise awareness about credit building as a way to help lift people out of poverty, said San Francisco Treasurer José Cisneros.

“They implemented something that has really changed the landscape, that has allowed people who were pretty much blocked from access to credit and financial services … a way to really enter the financial mainstream and to become financially successful,” Cisneros said.

In 2016, the MacArthur Foundation named Quiñonez a “financial services innovator” and awarded him a fellowship, commonly known as a “genius grant,” for creating a pathway to mainstream financial services for people with limited or no financial access.

Quiñonez arrived in the U.S. as an undocumented 9-year-old by crawling through drainage tunnel across the border and went on to graduate from Princeton. He said his childhood made him appreciate the value of lending circles for people to support each other.

After Quiñonez’s parents died in his native Mexico, he and his five siblings, ages 7 to 15 at the time, joined relatives in San Jose. The siblings ended up living on their own in two-bedroom apartment downtown, going to school on weekdays and working at a flea market on weekends to pay their rent.

“That’s how we, you know, pooled our money together to survive,” said Quiñonez, one of millions of people who were able to legalize their status thanks to President Ronald Reagan’s 1986 immigration reform.

Participants building credit

In Jazzel Wood Sr.’s lending circle, participants picked numbers from a bowl passed around by MAF staffers to decide who would get the first loan, about $1,400.

Woods drew number 5, which disappointed him because he needs the money sooner, he said.

“The landlord is talking about evicting me right now, and I got two kids,” said Woods, who works two jobs as a counselor and a facility manager at teen group homes. “I’m just trying to keep up with the bills.”

But he still signed on the loan agreement. With the $1,400 loan and what he expects will be a boost to his credit score, Woods wants to start paying for classes so he can earn more money at work, and eventually open his own business.

“This is actually going to help me create my own group home and become my own boss,” said Woods, who completed a lending circle once before with MAF. “Everything went great, my credit score increased.”

Researchers at San Francisco State University who studied MAF’s lending circles found a 19-point increase on average for participants who already had a credit score. The boost is much larger — about 600 points — for most of those who initially lacked a credit score.

About a third of MAF’s clients did not have a credit history when they joined, according to the organization.

MAF’s lending circles also improved emotional well-being and financial confidence for participants, said Frederick Wherry, a professor of sociology at Princeton University, who has studied the program for five years.

That was in stark contrast to the more anxiety-producing experience of dealing with the subprime loans or payday lenders that typically service people with no or poor credit scores access, said Wherry.

“That may in fact be a battlefield in which, any minute now, you’re going to step on a minefield and have all your dreams sort of blow into bits,” he said.

MAF’s lending circles offer a different financial service, one that originated from the community, and gives borrowers more control and choices in an environment of respect, he said.

“It’s about well-being, and it’s about not suffering some of the indignities that come with not having a credit score,” Wherry said.

High repayments

To join a lending circle, participants must first complete an online financial training with MAF. The organization also works with borrowers who fall behind on payments, and covers those amounts for the other members of their lending circle.

But the vast majority of people pay back, which counters the notion that low-income people are risky borrowers, said Quiñonez.

“When people come together and decide how much they are going to be lending each other … they look each other in the eye and then make that sort of commitment to one another,” he said.

Dozens of nonprofits throughout the country now collaborate with MAF to organize lending circles in African American, Vietnamese, LGBTQ and other communities. While those groups gather potential participants and inform them of how the lending circles work, MAF operates its loan servicing software.

Since 2008, MAF says it has facilitated nearly $11 million in loans, with the capital coming from the borrowers themselves — a key difference from microloans offered by other institutions in a growing industry.